#20- How to Optimize an EA Without Curve-Fitting Your Soul

-

Posted by

You finally have a decent EA. It’s making money live. Equity curve looks healthy.

Then the devil whispers: “Just tweak a few parameters… imagine if it made 40% more…”

Three hours later you’ve run 47,000 optimizations. Found the “perfect” settings: +680% backtest, 4% drawdown. Go live. Three weeks later: -59% and crying.

Welcome to curve-fitting hell – the #1 reason good EAs turn into expensive fireworks.

In 2026 it’s easier than ever to over-optimize (faster computers, better data, AI tools). Which means it’s also easier than ever to blow up.

Let’s fix that before you sell your kidney for the next “holy grail settings.”

What Curve-Fitting Actually Looks Like (Spot It or Die)

| Symptom | Real Edge | Curve-Fit Lie |

|---|---|---|

| Backtest return | 80–250% over 5+ years | 800%+ with perfect curve |

| Max drawdown | 25–45% | Under 12% |

| Profit factor | 1.4–2.2 | 3.5+ |

| Number of parameters tweaked | 3–5 | 27+ with 0.1 increments |

| Performance on 2025 data | Similar to 2020–2024 | Drops 70%+ out-of-sample |

If your optimized version looks too good to be human → it isn’t.

The Only Optimization Method That Works in 2026: Walk-Forward Analysis

Forget brute-force genetic nonsense.

Real pros do this:

- In-Sample Optimization Optimize parameters on 2019–2023 data.

- Out-of-Sample Forward Test Freeze parameters. Run on 2024–mid-2025 (never seen by optimizer). If performance drops >35% → trash settings.

- Re-Optimize Slide window forward: optimize on 2020–2024.

- Forward Test Again On mid-2025–now.

- Repeat 4–6 cycles Only keep parameter ranges that survive every single out-of-sample period.

Takes days, not hours. But the result actually works live.

My Personal 2025 Optimization Disaster (Learn From My Tears)

EA: Range Reaper (mean-reversion) Original settings: +94% 2023–2024 live Optimized aggressively on 2020–2024 data → backtest +380%, DD 7% Live Jan–Jun 2025: -64% Why? Optimized for the most ranging period in 20 years. 2025 volatility came → robot choked.

Lesson: optimizing for perfection = preparing for extinction.

The Lazy (But Honest) Optimization Rules for 2026

Rule 1 – Optimize ranges, not exact values. Example: RSI period 8–14 instead of exactly 11. Pick middle or random within range live.

Rule 2 – Max 4–6 parameters to optimize. More than that = you’re fitting noise.

Rule 3 – Include at least one major regime change. Your in-sample MUST include COVID crash, 2022 inflation spike, or equivalent.

Rule 4 – Robustness tests

- Change spread +0.5 pips → still profitable?

- Add random 1–3 pip slippage → still alive?

- Remove best 5 trades → still positive? Fail any = fake.

Rule 5 – The “Sleep Test”. If optimized settings make you think “this is too good,” delete them.

Rule 6 – Live forward only After walk-forward, run new settings on $1k–$5k live account for 3 months before scaling.

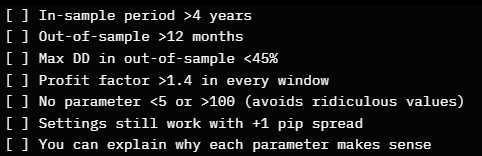

Simple MQL4/MT5 Optimization Checklist (Print This)

All yes? Deploy. One no? Back to demo.

Final 2026 Truth

Optimization doesn’t find better strategies. It finds settings that worked in the past.

The market doesn’t repeat the past. It rhymes… badly.

Your job isn’t to make the backtest perfect. Your job is to make the EA survive the future.

Curve-fit and die rich on paper. Optimize honestly and get rich in the bank.

Choice is yours.

Financial Disclaimer (The Over-Optimization Anonymous Edition)

This is not financial advice; it’s an intervention for parameter tweakers. If you spend more time optimizing than actually trading, you’re not a trader — you’re a backtest artist. One day the market will change and your perfect settings will become perfect losses. I’m not responsible when your “genetic optimized super bot” turns into a pumpkin at midnight. aristide-regal.com – where we optimize once, profit forever.

More updates : https://www.aristide-regal.com/blog/ and https://x.com/Aristide_REGAL

Leave a Comment