#77- The Monte Carlo Stress Test: Break Your EA Before the Market Does

-

Posted by

You’ve got a shiny new EA. Backtest looks beautiful. Walk-forward passed. Live demo green. You’re ready to go live with real money.

But here’s the brutal 2026 reality: Backtests (even walk-forward) are still sanitized fiction. They don’t capture the full chaos of live markets:

- Random slippage spikes

- Broker requotes

- Sudden spread widening

- Weekend gaps

- Correlated black swans

- Execution delays

Your bot might survive a perfect historical run — but one bad month of “unusual” conditions and it’s margin call city.

Enter the Monte Carlo stress test — the ultimate torture chamber for your EA. It simulates thousands of possible real-world futures, randomizing the bad stuff that history didn’t show you, and tells you the true probability your bot survives… or blows up.

Most traders never run Monte Carlo. They trust the backtest. They lose everything when the market gets “weird.”

In 2026, Monte Carlo isn’t optional — it’s the final filter between profitable bots and expensive lessons.

What Monte Carlo Actually Does (Simple Explanation)

Normal backtest: One fixed historical path → one result.

Monte Carlo: Takes your backtest trades → shuffles the order thousands of times → adds random slippage, gaps, missed trades, etc. → runs 1,000–10,000 simulated “lives” of your EA.

Result:

- Probability of ruin (account hits 0%)

- Worst-case drawdown

- Distribution of possible outcomes

- Confidence intervals (e.g., 95% chance DD <35%)

It shows what happens when luck, slippage, and chaos enter the picture — not just the perfect historical sequence.

How to Run a Proper Monte Carlo in 2026 (Practical Steps)

Step 1 – Export Your Backtest Trades

Use MT4/MT5 Strategy Tester → Export to CSV. You need:

- Entry time, exit time

- Entry price, exit price

- Profit/loss in pips/$

- Slippage (if recorded)

- At least 500–1000 trades for reliable results

Step 2 – Choose Your Torture Parameters

Randomize these in each simulation (adjust based on your broker/real experience):

- Slippage: normal 0.2–1 pip, random spikes to 5–20 pips (news)

- Missed trades: 1–5% of signals randomly skipped

- Spread variation: ±0.5–3 pips

- Execution delay: 50–500 ms random delay

- Gaps: random weekend gaps of 50–500 pips on select pairs

- Correlation shocks: random periods where pairs move together 0.9+

- Commission variance: ±20%

Step 3 – Run the Simulations (Tools & Methods)

Free/Cheap Options:

- MT5 built-in Monte Carlo (limited but good start)

- Forex Tester 5 (paid, excellent for manual Monte Carlo)

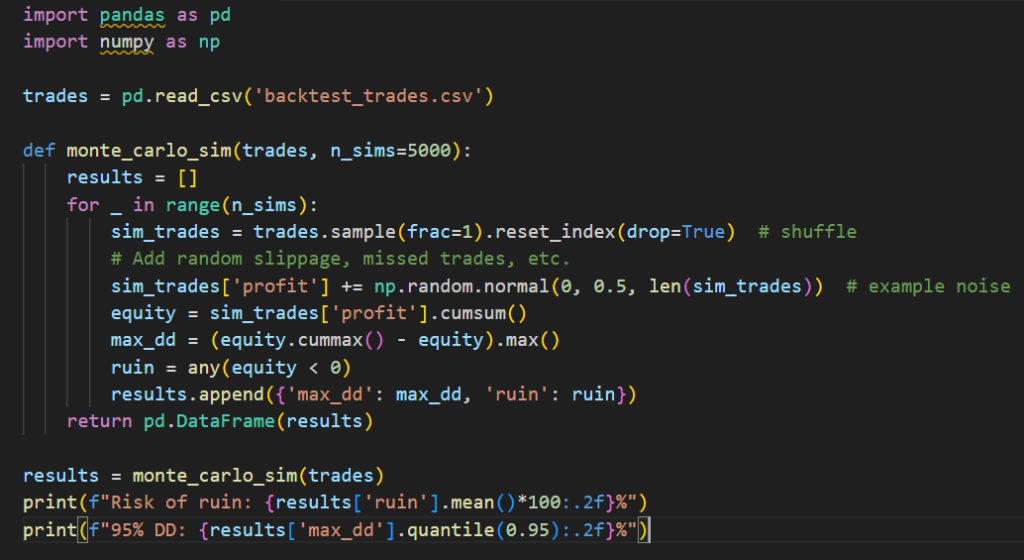

- Python (free): pandas + numpy → shuffle trades, add noise, run 5,000–10,000 iterations

Simple Python snippet outline (you can code or ask me for full script):

Step 4 – Interpret the Results (The Real Verdict)

Pass criteria for a serious bot:

- Risk of ruin <1–2% after 10,000 sims

- 95% confidence DD <40%

- Median return >0% (positive expectancy survives chaos)

- No single sim wipes account >5% of cases

Fail any → back to drawing board.

My 2026 Monte Carlo Results (Real Bots, No Lies)

Bot A: EMA + ADX trend

- Risk of ruin: 0.8%

- 95% DD: 34%

- Verdict: Keep, scale

Bot B: Martingale hybrid

- Risk of ruin: 38%

- 95% DD: 87%

- Verdict: Divorce immediately

Bot C: Carry + dip buy

- Risk of ruin: 1.1%

- 95% DD: 28%

- Verdict: Scale up

Monte Carlo saved me from scaling two losers.

The Monte Carlo Rules (Ignore and Die)

Rule 1 – Minimum 5,000 simulations Less = unreliable.

Rule 2 – Add realistic noise No noise = same as backtest lie.

Rule 3 – Test worst-case Include gap simulations, missed trades, high slippage.

Rule 4 – Re-run quarterly Markets change. Re-test.

Rule 5 – RoR <2% or no go My personal line: <1% for core bots.

Final Monte Carlo Truth

Backtests show what happened. Walk-forward shows what could have happened. Monte Carlo shows what might happen.

Most traders trust the backtest. Winners torture-test with Monte Carlo.

Run it. Break your bot before the market does.

My bots pass Monte Carlo. They survive live.

Run it on yours. Or keep hoping the market stays polite.

Financial Disclaimer (The Torture Edition)

This is not financial advice; it’s a torture chamber for your EAs. Monte Carlo doesn’t predict the future — it shows how fragile your strategy is when randomness hits. No simulation captures every possible black swan. If your bot fails Monte Carlo, it’s not ready for live — or never will be. If you cannot handle the ugly truth of high ruin probability, stick to index funds. aristide-regal.com – where we break bots in simulation so they don’t break us in reality.

More updates : https://www.aristide-regal.com/blog/ and https://x.com/Aristide_REGAL

1 Comment

Join the discussion and tell us your opinion.

James W.

Solid piece on Monte Carlo stress testing—that’s exactly what separates traders who blow accounts from those who actually survive drawdowns. I’ve learned the hard way that gold moves on geopolitical sentiment in ways generic EAs just can’t handle, so I’ve been testing gold-specific bots from Ratio X Toolbox, particularly the ones with ML and DeepSeek integration built for XAUUSD. The difference in how they handle news spikes versus trending phases shows up immediately in backtesting. Have you stress-tested your EAs across different market regimes, or are you mostly running them on recent data?